Remittances (or fund transfers) represent money sent by migrants living abroad to their families back home. This financial flow has become a vital source of income for many African countries. In fact, these transfers often exceed Official Development Assistance (ODA). But this money isn’t just used for daily survival. Increasingly, it is becoming a driver of economic transformation.

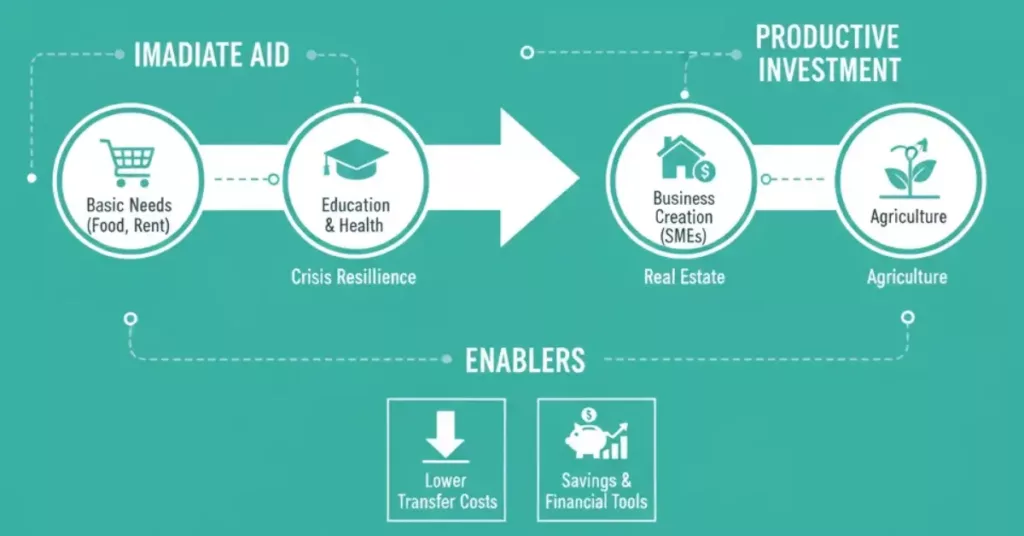

A Pillar of Daily Security and Well-being

Historically, the primary function of remittances is to offer immediate security to families.

- Supporting Essential Needs: Firstly, funds are used for food, rent, and clothing. This is crucial for reducing poverty in disadvantaged rural and urban areas.

- Improving Access to Services: Secondly, these transfers finance children’s education (tuition fees, supplies) and healthcare, which are often costly. Consequently, they improve human capital in the long term.

- Resilience During Crises: In cases of drought, illness, or local economic crises, money from the diaspora acts as a genuine social insurance.

In summary, remittances are an essential safety net that prevents families from falling into extreme poverty.

The Shift Towards Productive Investment

Beyond consumption, remittances are evolving. Thanks to greater awareness and adapted financial tools, a growing portion of this money is being directed towards investments that create lasting wealth.

- Business Creation: Many migrants send funds to start or develop small and medium-sized enterprises (SMEs), often managed by family members. For instance, this could be a retail business, a repair shop, or a small modernized farm. These SMEs create local jobs.

- Real Estate: Investment in the construction of houses or apartments is very common. Although this is often seen as a personal investment, it nonetheless stimulates activity in the building, transport, and materials sectors.

- Agriculture: The purchase of agricultural machinery, quality seeds, or irrigation systems is a productive investment that improves yields and food security.

Challenges and the Role of Digital Platforms

However, for remittances to fully transition from aid to investment, certain obstacles must be overcome:

- Transfer Costs: Fees remain too high in certain corridors (see the previous article). The lower the costs, the more money the family receives, and the greater the share available for investment.

- Lack of Savings Tools: Often, beneficiaries lack access to simple and secure savings or credit products that could transform their money into capital.

- The Role of Technology: This is where online money transfer platforms play a crucial role.

- They reduce fees, increasing the final amount received. It is in this same stride of technological revolution that the online money transfer platform Transfergratis offers its services.

- Furthermore, some platforms partner with local banks to offer dedicated savings accounts for diaspora funds, incentivizing beneficiaries to set aside money for long-term projects.

Remittances are an immense economic force for Africa. While their primary function remains assistance, their potential to stimulate productive investment is rapidly growing. Therefore, by facilitating access to fast and low-cost transfers, and by offering innovative financial products, the diaspora can become not only the support but also the engine of growth and sustainable development for its continent.

Try Transfergratis today and optimize your international financial flows! The Transfergratis platform is a free, fast, and secure money transfer service from Canada to Africa. Download the app on the Play Store or the App Store.

Create a free account to read this article

Join thousands of members who get exclusive access to expert guides, immigration tips, and the latest TransferGratis news.